5 Ways to Lower Your Health Insurance Cost In 2025.

Introduction

How to Save Money on Health Insurance Premiums: Practical Tips and Strategies

Health insurance is a critical part of our healthcare system, providing protection against the high costs of medical care. However, with premiums and other associated costs consistently rising, it can feel like a financial burden. While having health insurance is essential, it doesn’t mean you have to pay excessive premiums and deductibles. By following specific strategies, you can reduce your overall healthcare expenses without compromising on the quality of care you receive. This article will guide you through the steps to help you lower your health insurance costs, from shopping around for the best plan to taking full advantage of preventive care.

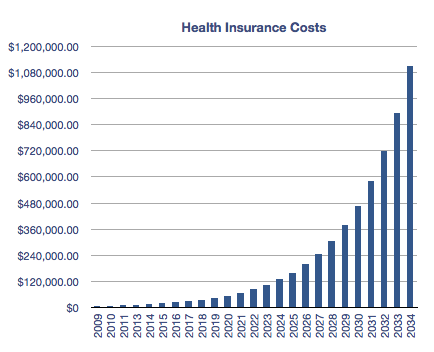

Why Health Insurance Costs Keep Rising

Understanding the underlying causes of rising health insurance costs is essential in finding ways to lower your premiums. The following factors play a significant role in driving up the cost of health insurance:

- Rising Healthcare Costs: As healthcare becomes more advanced, so does the cost of treatment. New medical technologies, treatments, and prescription drugs are often expensive. For instance, innovative treatments for conditions such as cancer or heart disease are not only costly but often require long-term care. These rising medical costs are passed on to consumers through higher insurance premiums.

- Aging Population: As the population ages, more people need healthcare, especially older adults who are more prone to chronic conditions. The increased demand for healthcare services directly leads to higher healthcare costs. In fact, people aged 65 and older typically require more medical care than younger adults, further driving up insurance premiums for everyone

- Prescription Drug Prices: Prescription medications are a major driver of healthcare spending. In recent years, prices for drugs—especially those for chronic conditions like diabetes, arthritis, and cancer—have skyrocketed. For instance, the price of insulin, a life-saving medication, has risen sharply in the past decade. These drug price increases add to the cost of health insurance premiums.

- Insurance Company Administrative Costs: Insurance companies must cover the administrative costs of processing claims, paying for customer service operations, and other business-related expenses. These costs are built into the premiums they charge. Additionally, health insurers often charge higher premiums to cover their profit margins.

- Lack of Competition in Some Markets: In some areas, particularly rural regions, there are limited health insurance providers available. Less competition means that insurers can charge higher prices because consumers have fewer options to choose from. This results in less market pressure to lower premiums and improve service offerings.

5 Ways to Lower Your Health Insurance Cost In 2025.

One of the best ways to lower your health insurance costs is by actively shopping around. Many people remain with the same provider year after year without comparing options, which may lead to overpaying for coverage. Here’s how you can compare and find the best deal for your needs:

Comparison Websites: Sites like HealthCare.gov, eHealth, and other online health insurance comparison tools make it easy to compare the premiums, coverage, and benefits of different insurance plans. These platforms allow you to filter options based on factors like your age, health status, location, and coverage preferences. This means you can find a plan that fits your health needs and budget without overpaying.

Evaluate Network Coverage: When comparing plans, it’s important to understand what healthcare providers are included in the plan’s network. Some plans may offer a broader network of hospitals and doctors, while others may limit you to a smaller group. If you have a preferred doctor or specialist, ensure they are included in the plan’s network to avoid costly out-of-network fees.

Look for Discounts: Many insurers offer discounts for factors such as non-smokers, gym memberships, or completing wellness programs. Some health insurance providers may also offer lower rates if you are in good health or if you have a family history of few medical claims. Don’t hesitate to ask about potential discounts or special promotions that could help reduce your premium.

Read Customer Reviews: Before committing to a plan, check reviews and ratings from current or former customers. Consider factors like claim processing time, customer service, and the ease of navigating the plan. A plan that looks affordable on paper might not be as effective if the insurer has poor customer support or limited provider options.

1.Choose a Plan that Fits Your Needs

It’s important to choose a health insurance plan that suits your specific lifestyle and health needs. While the lowest-priced plan might seem like a great deal, it may not provide the necessary coverage for your circumstances. Here’s how to find the best plan for you:

Consider Your Health Status: If you’re generally healthy and don’t require frequent medical visits, opting for a plan with a higher deductible but lower monthly premiums can save you money. However, if you have chronic conditions, are expecting surgery, or have a family that needs regular medical care, a plan with lower deductibles and more comprehensive coverage may be the right choice.

Tailor Coverage to Your Needs: Avoid overpaying for unnecessary coverage. For example, if you’re a single individual with no children, it’s unlikely that you’ll need comprehensive maternity care, so you can opt for a plan that excludes these services. Similarly, if you are young and healthy, you may not need extensive coverage for conditions like cancer or heart disease, so you can choose a more basic plan.

Review Your Family’s Needs: If you are covering a spouse or children, you’ll want to ensure that the plan provides adequate coverage for them. It’s important to check if pediatric care, vaccinations, and other family-related medical needs are covered. Consider the cost of adding family members to your plan and compare it to purchasing separate policies for each member.

2.Optimize Your Deductibles and Co-Pays

Balancing your deductible and co-pays is one of the most effective ways to lower your health insurance costs. Your deductible is the amount you must pay out-of-pocket for healthcare services before your insurance starts covering the costs, while co-pays are fixed amounts you pay each time you visit the doctor or receive a service. Understanding how to optimize these elements can significantly reduce your premiums:

Set an Affordable Deductible: Higher deductibles typically come with lower premiums. If you’re in good health and don’t expect to need frequent medical care, opting for a higher deductible may be a good option. However, make sure you can afford to pay the deductible if something unexpected happens, such as an injury or illness.

Co-Pays vs. Premiums: While higher co-pays mean you’ll pay more out-of-pocket when you visit the doctor or need medication, they often result in lower monthly premiums. If you don’t expect to visit healthcare providers often, this could save you money in the long run. However, if you anticipate frequent visits, you may want to consider a plan with a lower co-pay, even if it comes with a higher premium.

Review Prescription Coverage: Consider the cost of prescription medications when evaluating plans. If you take regular medications, look for a plan that offers good prescription drug coverage. Some plans may charge a higher co-pay for prescriptions or have a separate deductible for medications, so make sure you’re getting the best deal on your prescriptions.

3.Consider a High Deductible Health Plan (HDHP)

A High Deductible Health Plan (HDHP) is a health insurance plan that offers lower premiums but requires you to pay a higher deductible before the insurance company covers your medical expenses. These plans are a popular option for individuals who are generally healthy and don’t anticipate needing frequent medical care.

Lower Premiums: HDHPs are ideal for those who are healthy and don’t require much healthcare. These plans generally come with lower monthly premiums compared to traditional plans, making them an affordable option for people who are not expecting major health expenses.

Eligibility for Health Savings Accounts (HSAs): One of the key benefits of an HDHP is that it qualifies you to open a Health Savings Account (HSA). An HSA allows you to set aside pre-tax dollars to pay for medical expenses. The money in your HSA grows tax-free and can be withdrawn tax-free as long as it’s used for qualifying health expenses, such as deductibles, co-pays, and prescription medications.

Ideal for Healthy Individuals: HDHPs are best suited for people who are in good health and don’t expect to need extensive medical care. If you rarely visit the doctor, this type of plan can help you save money on premiums while still providing coverage in the event of unexpected health issues.

4.Utilize Preventive Care

How Preventive Care Can Lower Long-Term Costs.

Preventive care can significantly reduce your overall healthcare costs. Most health insurance plans offer preventive services at no additional cost to you. These services are designed to catch potential health issues before they become serious, and they can save you money in the long run by preventing the need for costly treatments.

Early Detection Saves Money: Regular check-ups, screenings, and vaccinations can help detect health issues like high blood pressure, diabetes, and heart disease early on. Catching these issues before they become major health problems can prevent expensive hospital stays, surgeries, and long-term treatments.

Free Preventive Services: Under the Affordable Care Act, insurance companies are required to cover certain preventive services without charging a co-pay, co-insurance, or deductible. These services include screenings for cancer, cholesterol checks, and immunizations. By taking advantage of these free services, you can stay healthier and avoid expensive treatments later on.

Better Long-Term Health: By investing in your health through regular screenings and preventive care, you can avoid the high costs associated with treating chronic diseases. Regular visits to your healthcare provider can help you manage risk factors and ensure you’re on the path to better health.

5. Consider Health Savings Accounts (HSAs)

What Are HSAs and How Do They Help Lower Insurance Costs

Health Savings Accounts (HSAs) are tax-advantaged accounts that allow you to save money for medical expenses. If you have a High Deductible Health Plan (HDHP), you can open an HSA and use it to pay for qualified medical expenses, including deductibles, co-pays, and prescriptions.

Tax Benefits: Contributions to your HSA are tax-deductible, meaning they reduce your taxable income for the year. The money in your HSA grows tax-free, and withdrawals for medical expenses are also tax-free. This provides an excellent opportunity to save on taxes while setting aside funds for future healthcare costs.

Flexibility and Portability: Unlike Flexible Spending Accounts (FSAs), which may have an expiration date or a “use it or lose it” policy, the funds in an HSA roll over year after year. This makes it a great tool for saving for future medical expenses, especially as you age and may need more healthcare services.

Lower Long-Term Healthcare Costs: By using an HSA to pay for medical expenses, you can avoid using your insurance for smaller costs, helping you keep your premiums lower. Additionally, HSAs can help you save for retirement since you can use the funds for qualified medical expenses in your later years.

https://medlineplus.gov/ency/patientinstructions/000870.htm

Conclusion

Lowering your health insurance costs is not an impossible task. By understanding the factors that affect premiums, shopping around for the best plan, optimizing your deductible and co-pays, and utilizing preventive care, you can significantly reduce your healthcare expenses. Consider options like HDHPs and Health Savings Accounts (HSAs) to help with long-term savings. Ultimately, the key is to choose a health insurance plan that suits your lifestyle and needs while also saving money wherever possible.

Frequently Asked Questions (FAQs)

- How often should I review my health insurance plan?

You should review your health plan annually during the open enrollment period. It’s also advisable to review your plan after major life changes, such as a new job, marriage, or the birth of a child, as these may affect your health insurance needs.

- Can I switch my health insurance during the year?

Generally, you can only switch your health insurance during the open enrollment period unless you experience a qualifying life event (e.g., marriage, divorce, or a new job). If you qualify for a Special Enrollment Period (SEP), you can change your plan at any time.

- What is a co-pay, and how does it affect my premium?

A co-pay is a fixed amount you pay for healthcare services, like doctor visits or prescriptions. Higher co-pays generally result in lower monthly premiums, but they can increase your out-of-pocket expenses if you visit healthcare providers often.

- What are the advantages of choosing a high-deductible health plan?

HDHPs offer lower monthly premiums and are ideal for healthy individuals who don’t expect to need much medical care. These plans also allow you to open an HSA, which offers tax benefits and helps you save money for medical expenses.

- Are there ways to save on health insurance without sacrificing coverage?

Yes! By shopping around, maximizing preventive care, optimizing deductibles, and considering HDHPs and HSAs, you can lower your insurance costs while maintaining adequate coverage for your health needs.

Leave a Reply